The platform, on a live book.

A walk through the cockpit, Q, and the risk families — running on the Future Bank demo dataset.

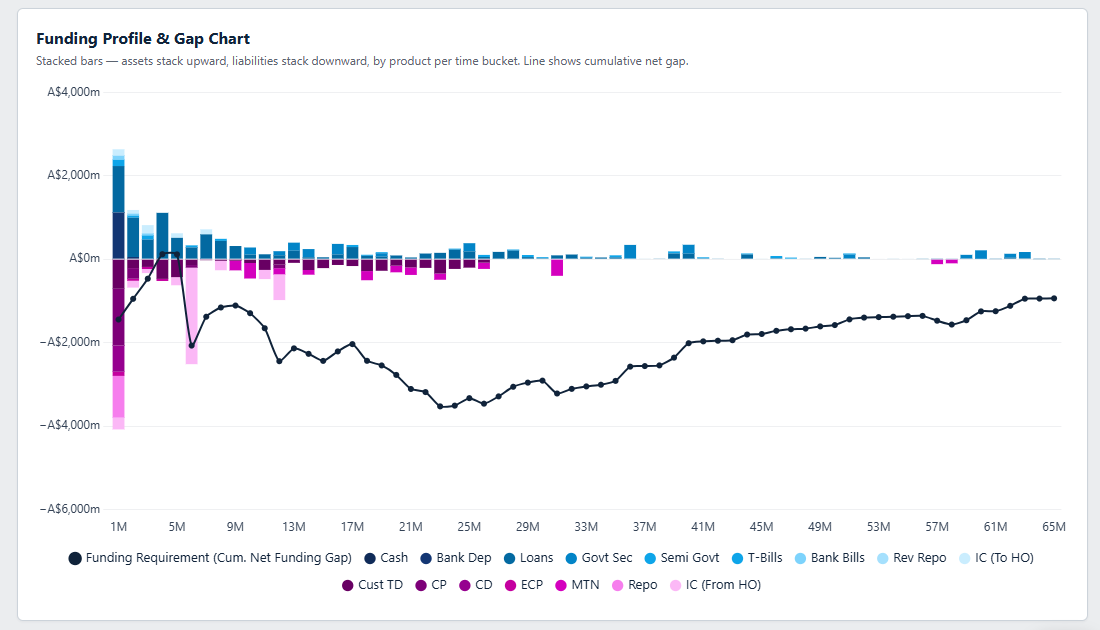

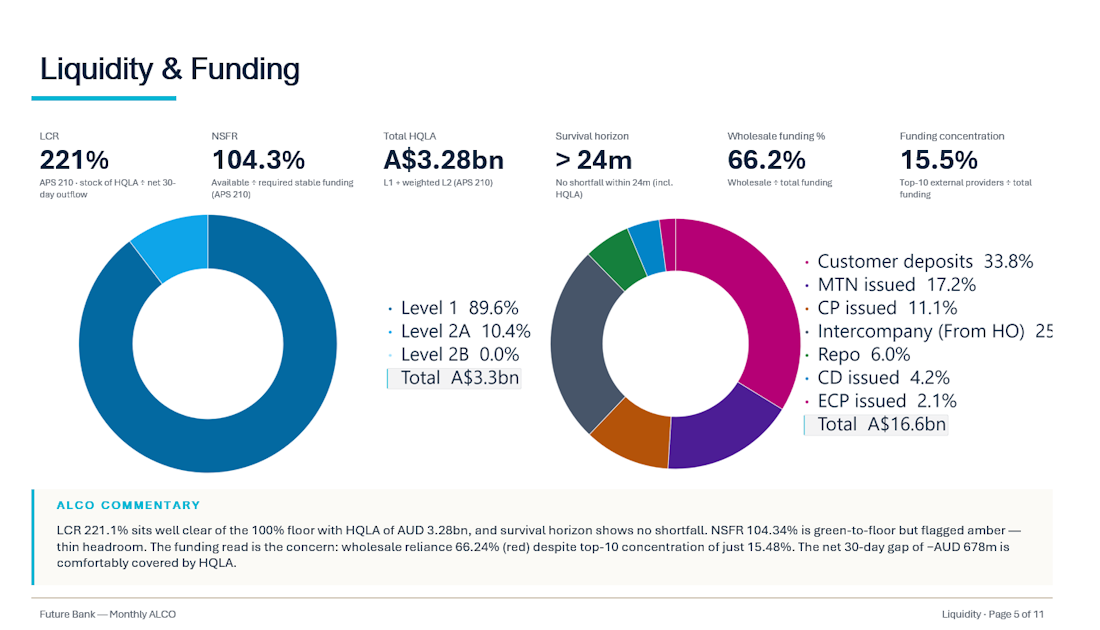

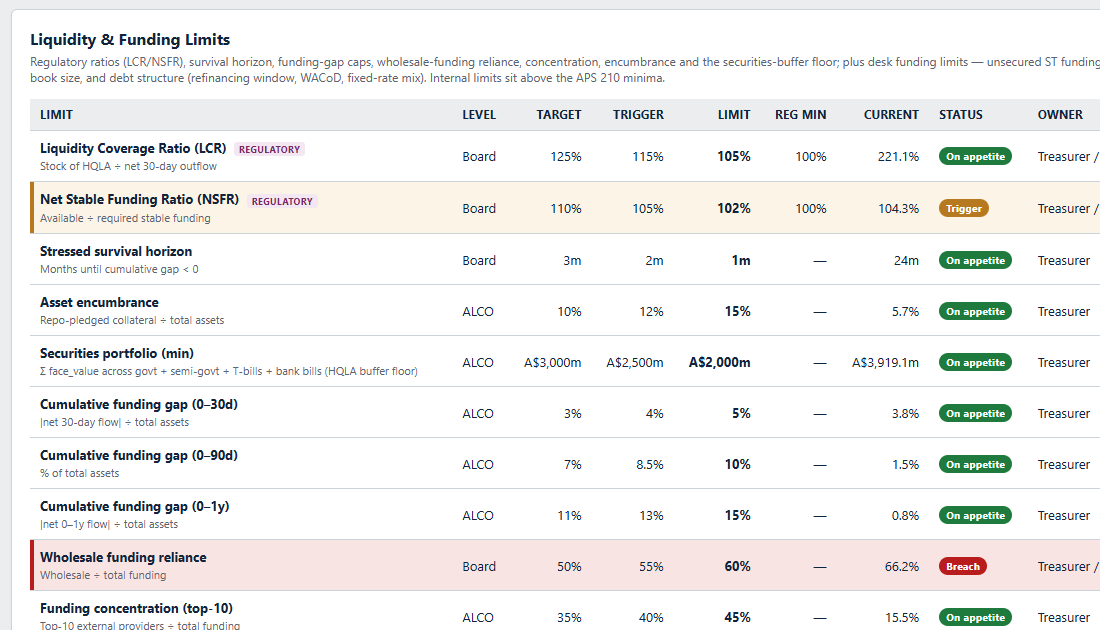

Funding gap & maturity ladder. The maturity ladder across every tenor bucket — funding gaps and the liquidity survival horizon, visualised at a glance.

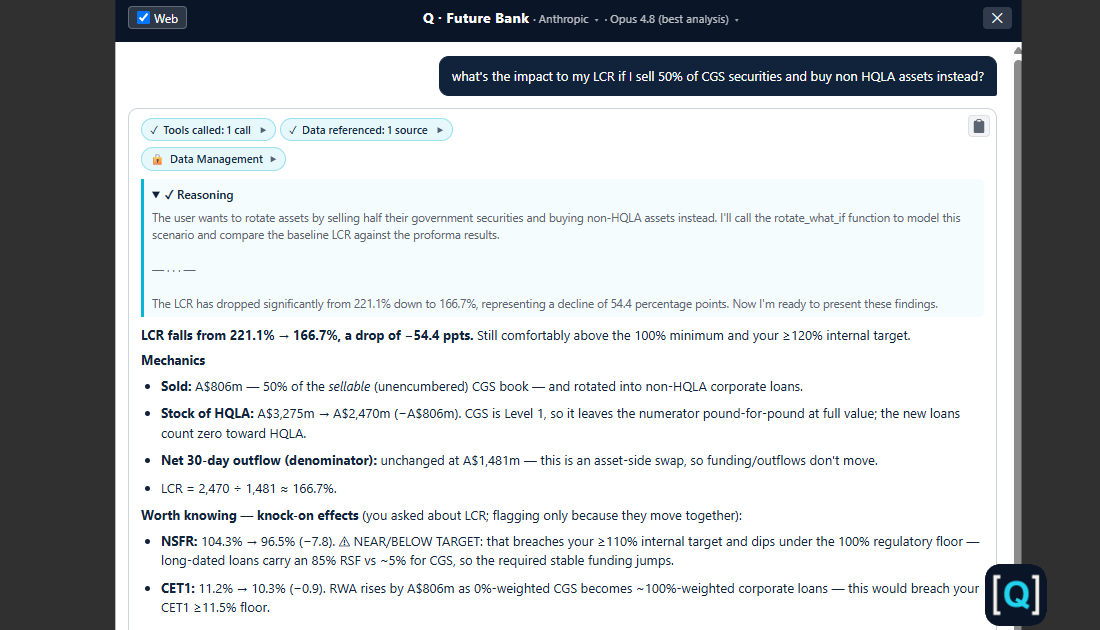

Q in conversation. Ask the whole book a question in plain English and get an analyst-grade answer that cites the exact positions.

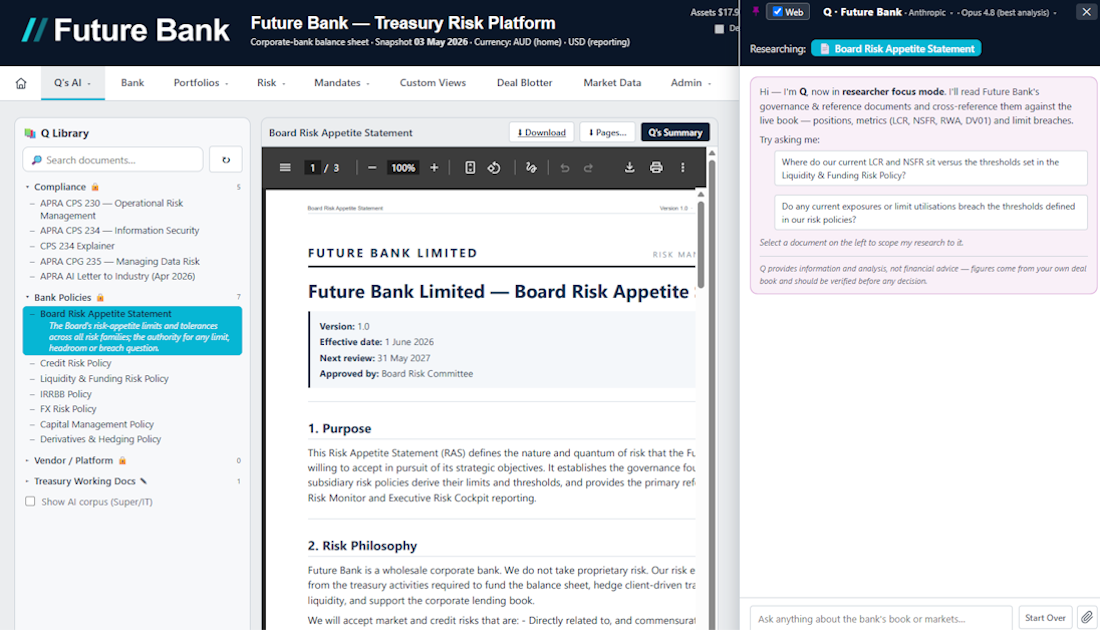

Q — policy library. Q reasons over your own limits, mandates and risk appetite — the policies encoded into the platform, not just the data.

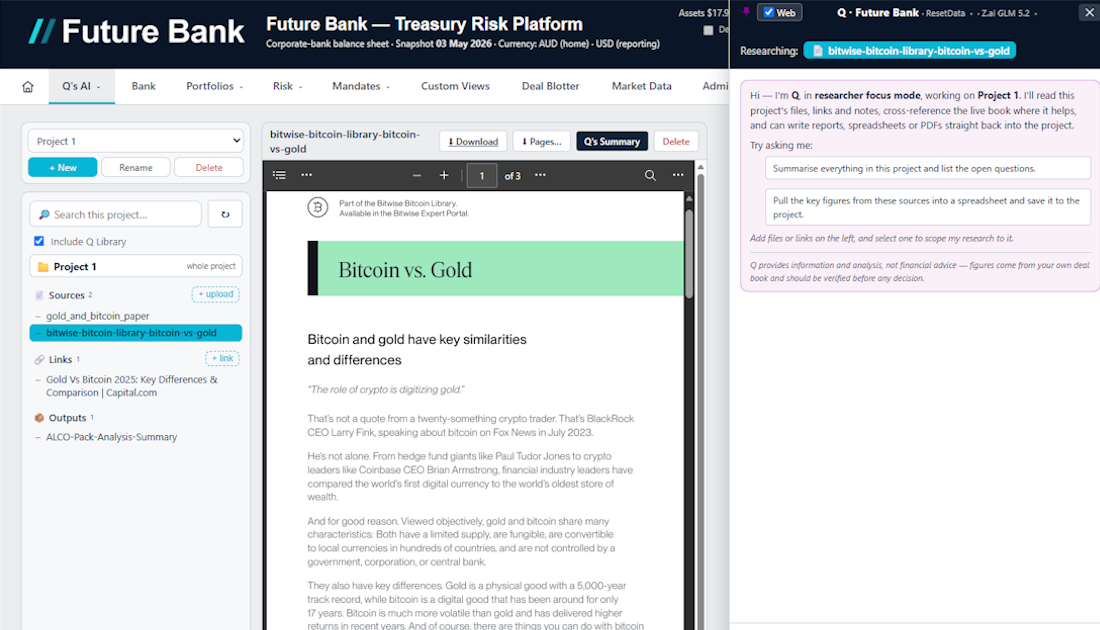

Q — saved projects. Spin up a funding review, hedge proposal or stress study and have Q build, organise and revisit the analysis.

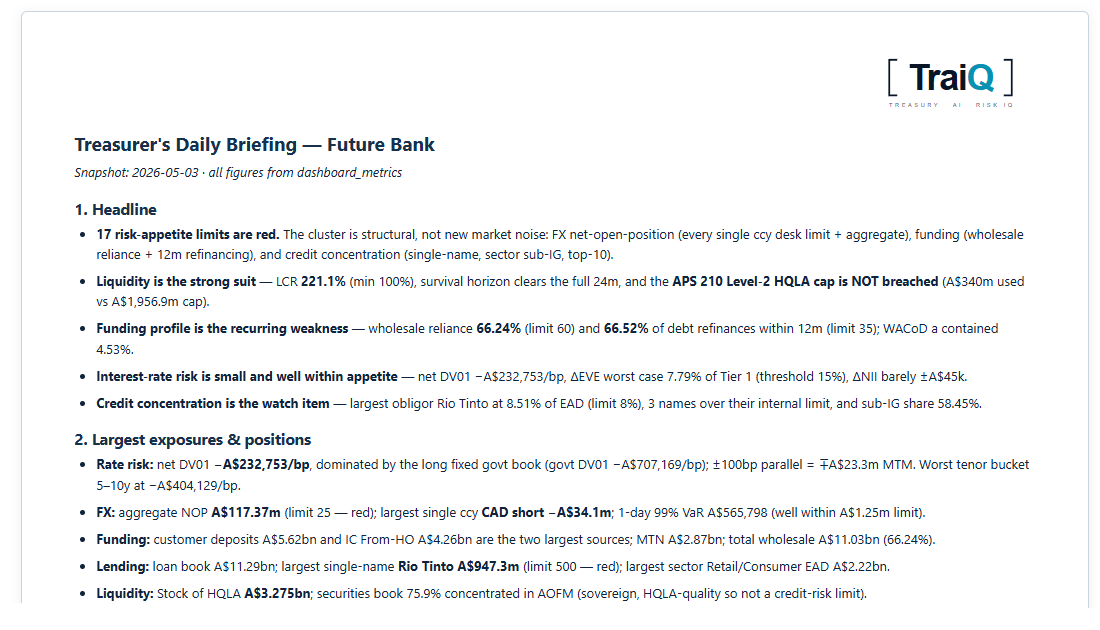

Q — daily briefing. A morning read of the book — overnight moves, breaches and watch items — drafted by Q before you sit down.

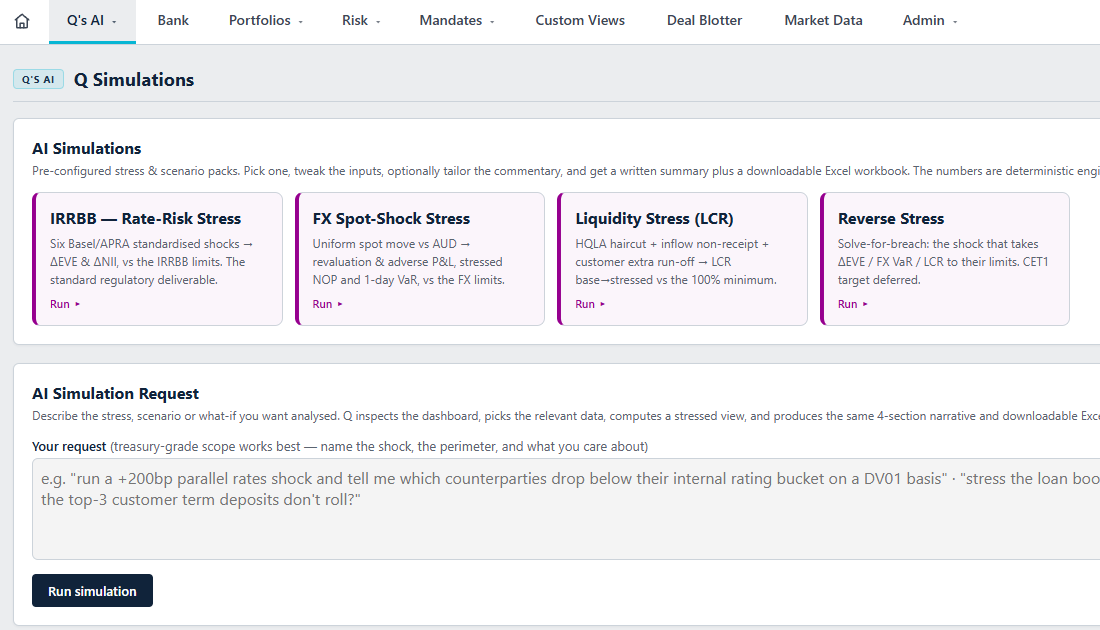

Q — simulations. Rate shocks, funding stress and counterparty default, run across the whole balance sheet in seconds.

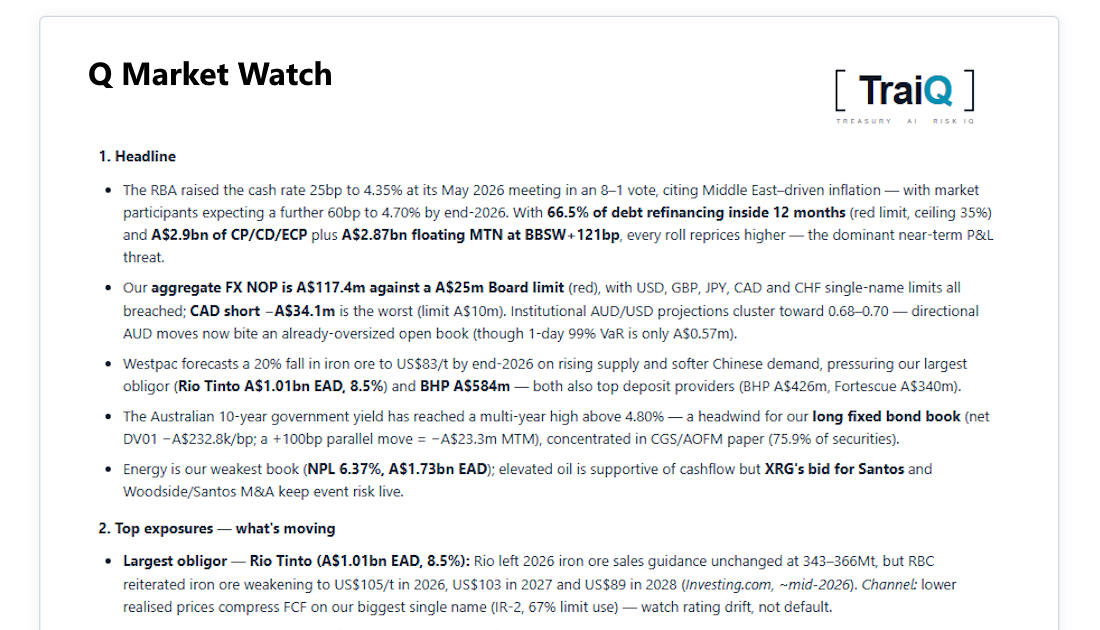

Q — market watch. Live market data alongside your positions, so Q can frame the book against where rates and spreads are moving.

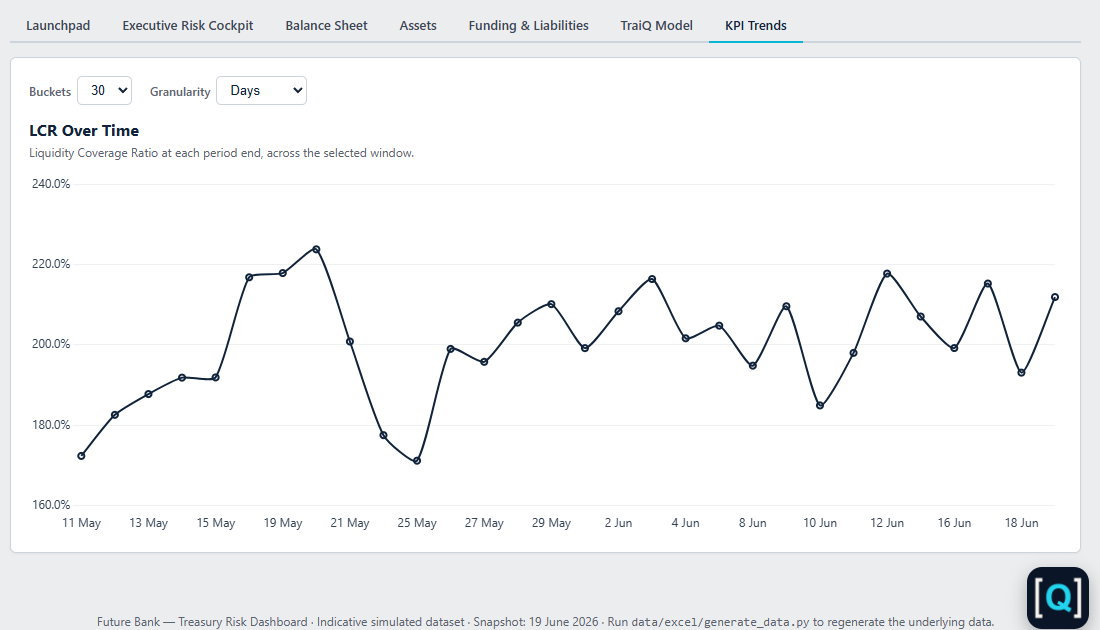

Q — time-series modelling. Project balances, ratios and exposures forward, and track how the book has moved across snapshots.

Q — ALCO pack. Board-ready ALCO packs generated from the live position and exportable for the committee.

ALCO pack. The full liquidity, rate and capital sections assembled into one committee-ready document.

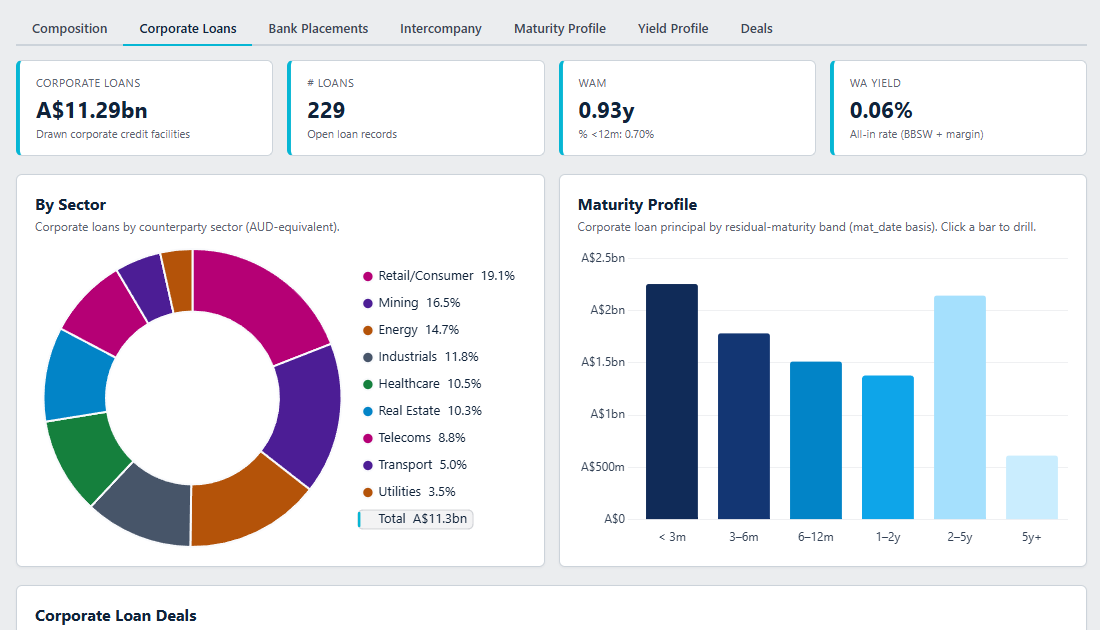

Corporate loans. The corporate loan book in detail — exposures, limits and credit quality, with drill-down to the facility.

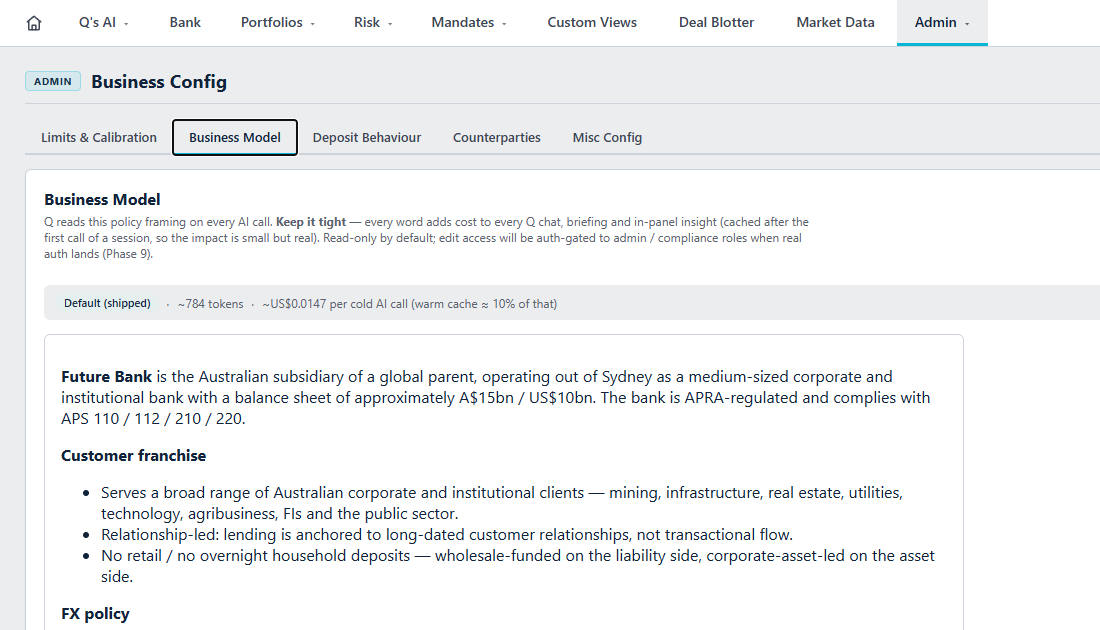

The balance-sheet model. Portfolios → products → risks → mandates: one coherent model of how the bank takes and manages risk.

Risk monitoring. Every risk family monitored live against appetite, with threshold alerts as ratios approach their limits.

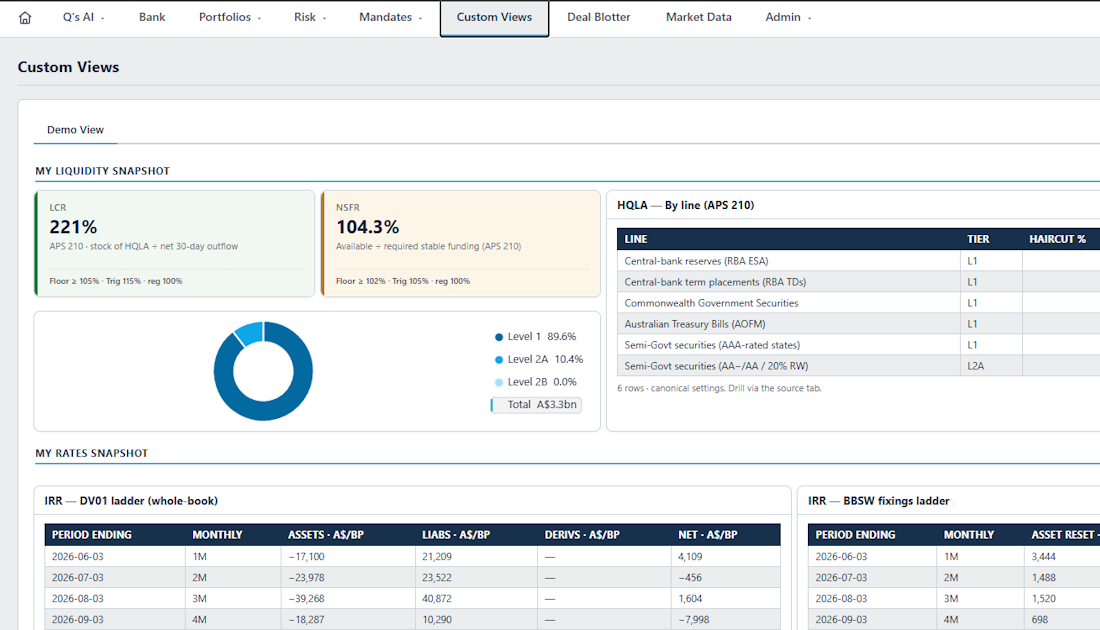

Custom views. Build the dashboards your desks actually use — per mandate, per portfolio, per role.

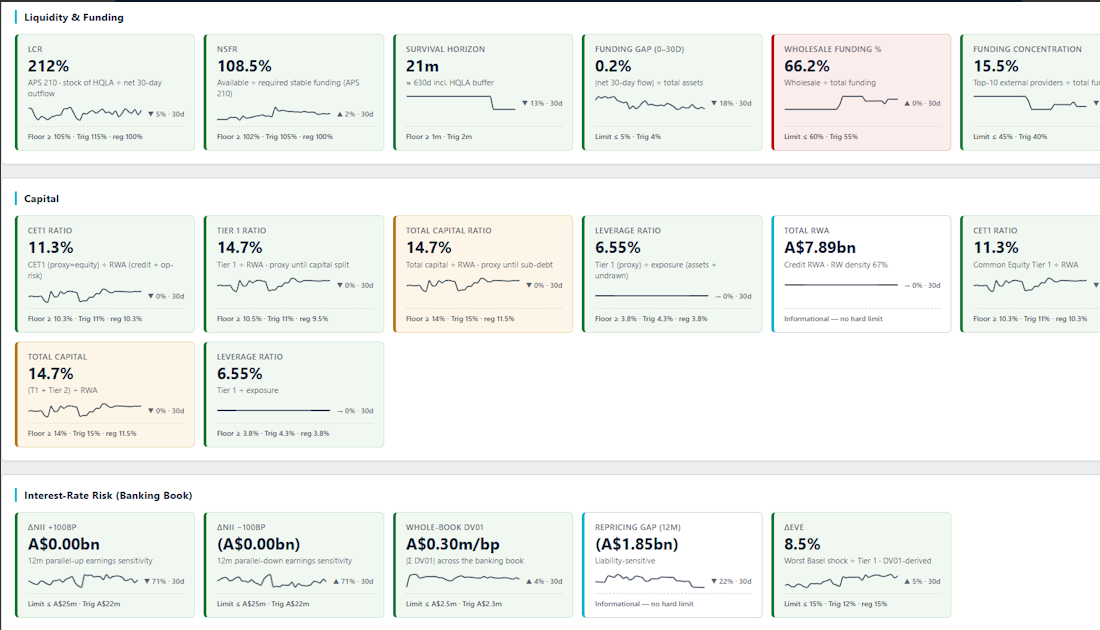

The risk cockpit. Every regulatory and risk metric calculated live, with Q docked alongside the whole book.

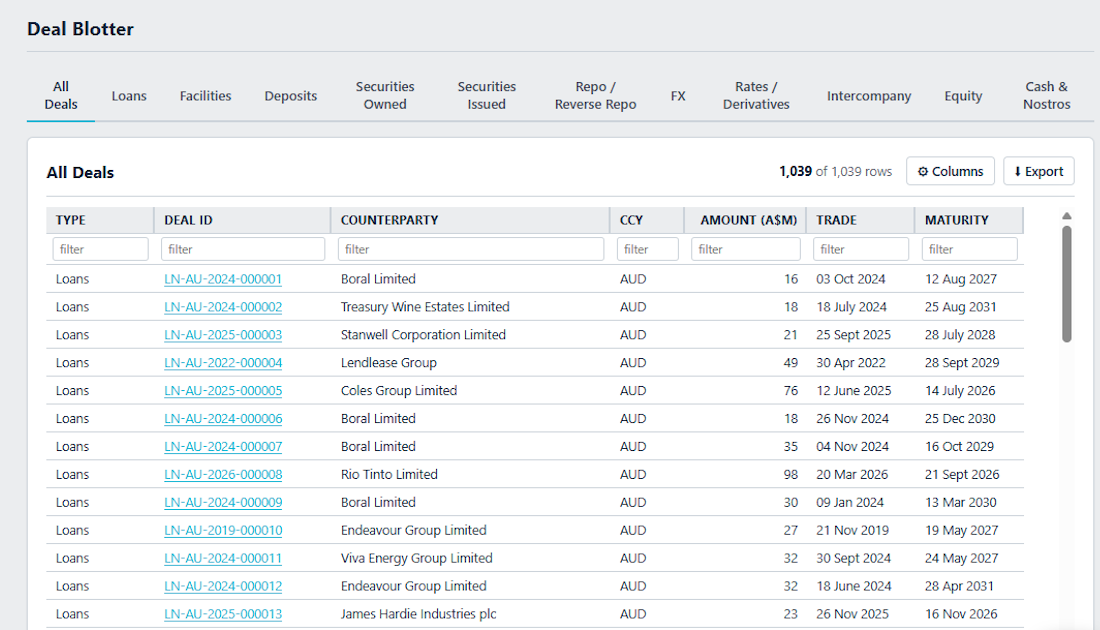

Deal blotter. The live deal blotter — every position across loans, deposits, derivatives, securities and FX, in one place.